Why Startups Fail? Research Project

Introduction

The goal of the project was to identify the reasons why startups fail. The data for the project was taken from the freely available startup post-mortems. The post-mortems were written by the startup founders and describe the main reasons for failures. A detailed overview of the research and lessons learned were published on medium.com and read by 50,000+ readers. It was written as a blog article and not as an academic paper, hence the writing style. Based on the insights gathered from the research, a startup checklist was created. The startup checklist is the summary of steps of how to build a startup and at the same time to minimize the risk of a startup failure.

Executive Summary

Here is an overview of the results gathered during the research project.

- It took an average of almost three years for a B2C startup to fail, and almost four years for a B2B startup to fail.

- 50% of B2C startups failed due to lack of market. The same goes for B2B, at a rate of 44%.

- Reason #2 for B2C startup failure was poor marketing (29%). Only 7% of B2B startups failed due to poor marketing.

- 17% of B2C startups hadn’t validated their ideas. B2B startups did a better job; only 3% hadn’t performed validation.

- 16% of B2C startups, and 20% of B2B startups, ran out of cash.

- 10% of B2C startups failed due to poor product. In comparison, only 3% of B2B did so.

- 1% of B2C startups failed because of problems with a third-party solution they had built on. In total, 10% of B2B startups failed because something happened to their third-party partner (e.g, Instagram has switched off its API for a specific product).

- 14% of B2B startups had problems with teams or investors, due in large part to the fact that many B2B startups are externally financed.

Main Article

Disclaimer: It was written as an article and not as an academic paper. The main target audience were startup founders, geeks, readers from medium.com. Please excuse the use of the language. Nevertheless, the research is based on real facts.

In 2009 I started a consulting business. It generated mid six-figures in revenue. It was small but very successful. I tried to understand the factors of my success. I thought that those factors were my domain expertise and hard work. I was sure that domain expertise and hard work is enough. So, I launched two other startups: Dataxient, where developers have stolen our code and Clever.do, that has failed to generate significant revenue.

I knew I need a better approach — one that would increase the odds of success. So my co-founder and I spent 300 hours over a number of weeks researching to find a solution. We sought to identify a single framework that would guide us towards success. It wasn’t easy, but we identified a combination of success factors. This essay explains what they are and how to apply them.

There are tons of books written from every possible prospective, from Lean Startup to Customer Development. I’ve read most of them. There are lots of models available, too, such as the Business Canvas Model. I know most of them as well. But none of them are applicable for me. Why, you ask? Too much information. Too many things we have no time for. If you start small, you need to keep your focus on just a few things. You need to know what is important! It feels like theorists and practitioners have developed these models. When it comes down to business, people make simple mistakes — even if they have read everything available about building a startup.

Let’s imagine your startup is a an airplane (a Boeing 737, to be exact). You, as founder and co-founder, are the pilots. Every pilot needs to perform specific set of checks — before starting the engines, before take-off, before approach and landing, and before shutdown. It’s a known fact that 95% of plane crashes are the result of people-made mistakes, not failures of technology. So, to help avoid these mistakes, every pilot who flies a Boeing 737 has a checklist (see example below). The checklist guides the pilot through every step in the process and helps them avert catastrophe.

I thought, why not create something similar? Taking off with a plane sounds similar to launching a startup. This is how we came to the idea of creating The Startup Checklist. To be honest, though, I had no clue how to create a structured checklist. I did some research, read a book, and discovered a powerful starting point — you need to start with the mistakes of others. People use this approach all the time in fields as disparate as medicine and aerospace.

Pabrai made a list of mistakes he’d seen — ones Warren Buffett and other investors had made as well as his own. It soon contained dozens of different mistakes, he said. Then, to help him guard against them, he devised a matching list of checks — about seventy in all.” — Atul Gawande from The Checklist Manifesto

We knew this was what we needed. So we started to work on The Startup Checklist. Our goal was to come up with structured information to

a) visualize the reasons for startup failures, and

b) create a list of checks to avoid those failures

We started to analyze failed startup stories, using Autosy.io, CD Insights, and Quora as our main sources of information.

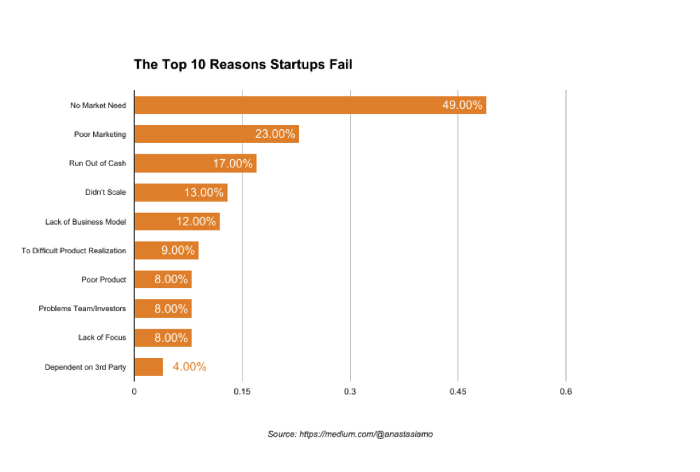

After a few weeks of researching, we identified some patterns. Our research showed that the most important factor for success, and, at the same time, for failure, was the market. Many of the failed startups we examined had several reasons for failure. But the market played the most important role. The figure below shows the top ten reasons for startup failures found in our research.

The market is the number one reason for failure. At the same time, it’s the most underserved topic in the whole startup field. People talk about building great products. They write about creating amazing working cultures. They show how to hack growth. But I haven’t seen many essays about how to find, analyze, and prove the market. I’m not talking about landing page signup; I’m talking about deep and thorough market analysis.

Before moving on to the discussion of each individual reason for failure, let’s review some short facts from our research.

It took an average of almost three years for a B2C startup to fail, and almost four years for a B2B startup to fail.

50% of B2C startups failed due to lack of market. The same goes for B2B, at a rate of 44%.

Reason #2 for B2C startup failure was poor marketing (29%). Only 7% of B2B startups failed due to poor marketing.

17% of B2C startups hadn’t validated their ideas. B2B startups did a better job; only 3% hadn’t performed validation.

16% of B2C startups, and 20% of B2B startups, ran out of cash.

10% of B2C startups failed due to poor product. In comparison, only 3% of B2B did so.

1% of B2C startups failed because of problems with a third-party solution they had built on. In total, 10% of B2B startups failed because something happened to their third-party partner (e.g, Instagram has switched off its API for a specific product).

14% of B2B startups had problems with teams or investors, due in large part to the fact that many B2B startups are externally financed.

#1 Your startup will die in three years

“I made the incredibly difficult decision to shutdown imercive. Three years, a lot of money, and all my passion had been invested in this company but it ultimately was not going to be the success I had envisioned.” — from Keith B. Nowak — Postmortem Of My First Company (A Reposting)

Paul Graham gave the advice to start a business before 38 years of age. After conducting my research for this checklist, I understand the reason why. If you are over 30, the time ticks. As we know, the success rate of startups becoming profitable is low. All the odds are against you. Therefore, by launching a startup you risk losing three years of your life. The older you get, the more difficult it becomes because the costlier lost years are.

Most of the people who failed wrote about their amazing experience. They don’t regret it, and will do it again. But in general, even if the experience will be amazing you still need to be prepared to lose three years of your life.

For the first version of our most recent startup, Clever.do, we spent $10,000 including marketing. After 2000 initial user registrations, we understood that we weren’t going to succeed. Even if we tried to pivot, there were no signs that the situation would change in our favor. Sam Altman has a basic rule for when to quit: “When you have tried all the ideas and it’s still not working you should quit.” This is how we made a decision to pull the plug.

Don’t think about pivots and all the other things people write about. Just set a rule: If X happens, or if Y doesn’t happen, you will pull the plug. Create a failure plan. Once the triggers are reached, the failure plan should kick in. At the same time, try to be persistent and reach your goal. Do whatever is needed. Rewrite the code, hire and fire people. Change the product, make tough decisions, or get external money.

#2 Lack of market will kill your startup

Adrian’s team failed to prioritize the customer market. They overlooked the fact that parents are satisfied with Facebook. They didn’t care much for secure and private upload and sharing — they just wanted something fast and basic. To put simply, there was no market for Remember. — from Adrian Tan: Why My Startup Failed And What I Learned From It — JFDI.Asia

If there is no market for your product, no one will buy it. People don’t care about you or about how amazing your product is. For me, it was interesting to see that only 8% of startups failed because of a poor product. It seems that most of the startups had managed to build at least an OK product. As I wrote, the market is the most underserved topic in the whole startup field. People pay less attention to the market itself than to almost any other aspect of starting a company.

Marc Andreessen once wrote that the market matters most. After our research, I see why. You can change the product and the team, but not the market. As Andy Rechloff said, “If you are in a bad market with a good product = market wins.” Let me rephrase: a bad market will kill you, even with a good product.

In my consulting business, I was in a great market. I didn’t realize that the main success factor was the market itself. Sure, domain expertise and hard work helped me a lot, but without the market, I would have been nothing.

Contrast that with my most recent startup, Clever.do. My co-founder and I thought we were in a great big market — the productivity market. We picked a subsegment (personal performance). But it turned out that people were simply not willing to invest their time and money. There was no market in the niche we picked.

Pay attention to the market first. Here’s one simple rule for spotting a great market. Try to find categories with a lot of competition. A lot of competition means lots of money. If there is no competition visible, or if the competition is very weak, be suspicious. Don’t jump into the mode of building a product. Do further investigation to get a full understanding of the market landscape. I strongly prefer to go into a market with many competitors. Frankly, I would skip a market that is devoid of competition.

A market opportunity does not necessarily equate to a market need. Another difficulty here is that being first and having no competition looks fantastic at first glance because you feel like you have discovered something no one else knows about. However, sometimes there is a reason no one else is around. — from Keith B. Nowak — Postmortem Of My First Company (A Reposting)

#3 You need to have a plan for how to make money

Another important point is the need to be a salesman. If you are not the Salvation Army, you need to earn money with your company. Don’t wait too long to sell your product or commercialize your service. If you don’t have the new super-viral-service, you have to go to your customers, and to the media, and sell your product. — from Maximilian Meyer from How to Fail a Startup

You need to have a plan for how to generate money from the outset. I’m not talking about planning the numbers. The numbers will be wrong. I did it often and failed, because no one knows what will happen in the future. But you need to understand how to make money with your startup. Why am I telling you this? Because the concept of building a product first and then figuring out how to make money later is wrong. Startups are not about having fun. Startups are real businesses. If you don’t know how to make money, call it your hobby.

If you don’t understand how to make money with your startup, think harder and find an answer. Look at your competition to see how they do it. Find out everything you can about them and copy their business model. If you still don’t know, you had better pause for a moment. Don’t go into solution mode without knowing how to make money. It won’t help you!

#4 You need to know how to build stuff

The second thing was the time taken. I had no tech knowledge when I started HitMeUp, so not only was I unable to build the MPV myself, I also didn’t know how to hire someone else to do it. That meant that twice I paid for developers to build Version 1, and twice I got ripped off and had to start over. — from Trillion Fund Hitmeup Post Mortem.

If startup founders have no clue how to build stuff, their chances of running out of cash are high. One of the reasons for this is their inability to assess the quality of the work in question. The development will take too long. It will become expensive. Code and product quality will be shit. You will need to rewrite the whole code, and so forth. Don’t try to create something amazing from the beginning. You need the first version to test the market. Limit your spending. Even if the first version is bad, ship it!

If you don’t know anything about technology or how to build stuff. I recommend you find a partner, mentor, or co-founder. Otherwise, you will get ripped off.

#5 You are likely to run out of cash

Our demise happened because we tried to scale prematurely at RewardMe. We attended expensive conferences and trade shows, booked flights to meet with clients, added several people to the growth team, bought tons of hardware before we sold it to clients (so we had to hold inventory), and delegated customer support before finding product market fit. Though on paper we had tremendous progress, we brute forced our growth and never established a stable product or a scalable customer acquisition channel — from Jun Loayza Premature scaling killed us — The Hustle is Real

Many of the failed startups made mistakes in managing their money. They spent tons of cash on offices, expensive trips, hardware and more. For example, If you need an office, do it like Marc Andreessen suggests: Spend your budget on two things first — ergonomic chairs and high-quality monitors for your team. The rest can be bought cheaply from IKEA. Try to save as much money as possible. To increase your runaway rate, which is equal to the lifetime of your startup, you may need every cent left in the bank.

Another thing which these failed startups often had in common was that they over hired. By hiring too many people you will create problems with communication. As the team size increases, communication and decision making slows down. Still, if you need more people than you and your co-founder, follow the “Two Pizza” team principle from Amazon. To stay nimble and agile, Amazon creates small teams. The maximum team size is 5 people — no more than can be fed by two pizzas (and no cheating with XXL pies!). It’s one of the key success factors behind Amazon’s innovation.

When we worked on Dataxient, we had four founders and four developers. It made our communication complicated. We couldn’t even run proper daily standup meetings. It was a disaster for everyone.

Mo’ people, mo’ costs, mo’ problems.

#6 You need to know your business well.

When you don’t know an industry, it’s very easy to spot a gap in it. It took us (largely people from a tech background) two years to fully understand the market we were entering. When we did, we realised that the gap we were trying to fill didn’t actually exist. If you haven’t been working in an industry, full time, for more than 24 months — it’s pretty safe to say you probably don’t understand it. Think carefully about that before you dive into your „I can’t believe nobody has done this yet“ startup idea. — from John O’Nolan Travelllll Post-Mortem

If you aren’t an expert in the market you want to enter, don’t enter it. There is a high chance you will miss either the market, the audience, or the product. You need to be 100% sure that you have enough knowledge.

When I started Dataxient, I knew the data visualization market. I knew the gaps in the market, and I knew the real customer pain-points. I had worked with data visualization on a daily basis. But, unfortunately, we were ripped off by our partners. They stole the whole source code and everything related to the project. However, since they had no fucking clue about the visualization market they failed to build and sell the solution.

There is a shortcut I use in situations where I don’t know something: I spend two weeks researching and reading about the specific topic. After that, I typically find that I’m smarter than 99% of other people about that topic, who haven’t done such intensive research. This shortcut can help you to evaluate an industry or a niche.

#7 Let other people steal your idea.

Discuss your startup idea not only with friends, but also other people who are strangers to you. I promise that you will definitely learn a lot here. The concept of your idea getting stolen is 99.99% impossible. Visit bar camps, hackerspace, geek terminals and bounce your ideas to different people. We failed to do this step and hence overestimated the Singapore market. We found that the Singapore market for such a service turned out to be very small. People are SMS crazy in Singapore, but that does not mean that they were ready to pay for the service. — from Vijay Ganesan Tech in Asia — Connecting Asia’s startup ecosystem

Stress-test your ideas as often as possible. You will learn a lot about potential usage and the pain-points your potential customers have. If you start something innovative, there could be another problem, though: the market may not be ready for it. Talk to everyone you can to pitch your idea. Don’t be afraid that someone will steal it from you. As we see from the examples above, it takes a lot of time and energy to build a profitable startup.

Again, don’t be afraid that someone will steal your idea. Be afraid to fail in three years and lose a lot of money because you haven’t done your homework. Your homework should be to validate your idea. Talk to everyone — tell everyone what you want to do.

#8 Get your MVP into the hands of your customers

We spent way too much time building it for ourselves and not getting feedback from prospects — it’s easy to get tunnel vision. I’d recommend not going more than two or three months from the initial start to getting in the hands of prospects that are truly objective. — from David Cummings Post Mortem on a Failed Product

Many startups that failed spent a year or more developing the first version of their first product — often, even if the product wasn’t complex. How crazy is that? They wanted to create the perfect experience from Day One. When they finally launched, they were too late to get feedback from the market. Either they had lost all their money or they were discouraged. If you work on something for a year without releasing it to your users, it’s so fucking demotivating for your team.

Since the first version of your first product will be shit, my suggestion is to set a clear deadline. At this date, you will ship the product regardless of its status. The first version of Clever.do was shipped after three months of development. We learned a lot from our users, but we also understood that no matter what we did our startup will not take off. It helped us to make a decision to pull the plug early.

While building the first version, your goal is to learn from the market. Don’t think about making money. Try to learn as much as possible from the market. Get insights and make fast decisions. Don’t be afraid to pull the plug. The startup is just a startup — it’s not your whole life, and no one will die if you kill it. You can start something else again.

#9 A value proposition will help you to stay focused.

Value propositions need to be super clear, straightforward and deliver (or at least claim to deliver!) immediate results. Tying value propositions to making more money is best. Saving money is second best. Everything else is tertiary… — from Ben Yoskowitz A Postmortem Analysis of Standout Jobs

If you know your value proposition, then you know what you are working on. It’s hard to come up with a compelling value proposition. Many startup founders have written about their experiences, but few have touched on value proposition. Value proposition will help you to stay focused. It will help you to communicate with your potential customers. It will increase your conversion rate and save your startup. Take it seriously and test different versions of it.

“Importance of a clean message. Distil your idea down to a simple message that a 5 year old would get in under 3 seconds — that’s about how much attention people are going to give you. This should be done before anything else.” — from Robert Tregaskes Shnergle Post Mortem

It was difficult to finish this essay. I started over and over again. I wasn’t sure how to describe most of my personal learnings. I had so many mixed feelings, from sadness to happiness. We spent a couple of weeks studying all these cases, and during that time I realized one thing: you need to be born as a founder.

Checklist Download

The gathered facts were used to create a startup checklist. The main reason to create a startup checklist is to help founders to minimize the risks. The startup checklist is available for download here.

Conclusion

The main reason for startup failure is the lack of a market. The second reason is poor marketing. It is important to emphasize both points. Based on the insights, a startup should focus on the market and not the idea. It’s the inversion of control. A startup needs to create a product that customers want and not a product that startup wants.

Refernces

- Original Medium Article by Dimitri

- Original Medium Article by Anastasia

- Sources of startup post-mortems:

- https://www.techinasia.com/4-mistakes-made-and-lessons-learnt-by-vijay-of-smsnoodle

- https://www.facebook.com/notes/eventvue/eventvue-post-mortem/470086850385

- https://calbucci.com/sampa-from-birth-to-death-dc3d4c83b9fe

- http://blogs.wsj.com/venturecapital/2009/07/14/turning-out-the-lights-baby-boomer-social-network-teebeedee/

- https://venturebeat.com/2009/04/29/10-lessons-from-a-failed-startup/

- http://brodzinski.com/2009/01/lessons-learned-startup-failure-part-1.html

- http://innonate.com/2008/06/19/bricabox-goodbye-world/

- https://techcrunch.com/2008/05/20/anatomy-of-a-failure-lessons-learned/

- https://hitechstartups.wordpress.com/2008/05/23/lessons-from-kiko-web-20-startup-about-its-failure/

- http://mediashift.org/2007/07/co-founder-potts-shares-lessons-learned-from-backfence-bust197/

- https://venturebeat.com/2007/01/19/bitpass-croaks-is-this-the-end-of-micropayments/

- https://audreyledoux.com/2016/10/25/spinvite_postmortem/

- https://np.reddit.com/r/Entrepreneur/comments/504wjz/we_hear_a_lot_about_the_success_stories_on_here_i/d71d1vo/

- http://www.startupnews.com.au/2016/05/30/killed-latest-startup/

- https://www.ft.com/content/8b1f84de-0230-11e6-99cb-83242733f755

- https://sungwoncho.io/lessons-from-building-vym/

- https://www.linkedin.com/pulse/what-founders-can-learn-from-spoonrockets-demise-caroline-fairchild?trk=eml-b2_content_ecosystem_digest-hero-14-null&midToken=AQEMlmMXBI0fCg&fromEmail=fromEmail&ut=3mSveUHZS7Rn81

- http://blog.eulergy.com/posts/eulergy-closes-it-s-digital-doors/

- https://medium.com/@mirceagabrieleftemie/the-highs-and-lows-of-entrepreneurship-5e786cac9d59

- https://yourstory.com/2015/11/lessons-failing-startup/

- https://backchannel.com/why-homejoy-failed-bb0ab39d901a

- http://www.geektime.com/2015/10/25/popular-israeli-app-launcher-everythingme-closes-down-most-of-staff-let-go/

- https://venturebeat.com/2015/08/10/gowalla-founder-josh-williams-shutters-last-a-company-that-made-apps-to-help-you-go-outside/

- https://www.techinasia.com/danny-taniwan-alikolo-startup-failure-indonesia

- https://medium.com/circa/farewell-to-circa-news-7d002150f74b

- http://taleoftales.tumblr.com/post/122153044077/and-the-sun-sets

- https://medium.com/startup-lesson-learned/5-reasons-why-my-iot-startup-failed-19c5537e61e1

- https://medium.com/@aszig/let-it-go-let-it-go-sunset-of-my-first-startup-ratemyspeech-co-f79b1d72c482

- https://medium.com/@Santafebound/my-startup-failed-and-this-is-how-it-went-down-c9654d23c5be

- http://www.axs.com/search?q=How+to+Learn+From+Your+Mistakes+in+a+Tech+Startup+

- https://medium.com/inside-wattage/well-we-failed-77e795e16ecf

- http://www.jfdi.asia/blog/adrian-tan-why-my-startup-failed/

- http://tech.eu/features/4346/kolos-kickstarter-story/

- https://medium.com/secret-den/sunset-bc18450478d5

- http://dopeboy.github.io/Lessons/

- https://medium.com/@stereomoodteam/the-last-song-for-stereomood-s-founders-b9c2b2ac0cf0

- http://www.gamasutra.com/blogs/IvanMir/20150217/236560/Postmortem_Traps_for_Friends__our_attempt_at_fair_IAP_multiplayer.php

- https://medium.com/startup-autopsies/case-study-of-a-failed-startup-37db342df2bf

- https://medium.com/gokart-labs/the-idea-is-dead-long-live-the-idea-b9bc132d6f50

- http://melissatsang.com/2014/01/15/cusoy-a-postmortem/

- http://michalsobel.com/en/experiences/the-idea-of-giving-up-is-worse-than-of-it-killing-me-how-150-000-post-it-came-to-be

- http://svedic.org/personal/zagreb-cohousing-fail

- http://www.startupnews.com.au/2014/10/29/startup-post-mortem-keep-fit-stay-sane/

- https://medium.com/@andershsi/3-reasons-why-my-tech-startup-failed-fa19919a565a

- http://blog.getsocial.io/5-mistakes-i-made-launching-a-startup/#gs.28465420ef1244cabdfe053383c1ba1a

- https://medium.com/adventures-in-consumer-technology/99-problems-but-a-bit-aint-one-why-my-startup-failed-9367978a6bf3

- https://medium.com/@michalbohanes/seven-lessons-i-learned-from-the-failure-of-my-first-startup-dinnr-c166d1cfb8b8

- http://netonomy.net/2014/10/26/the-rise-and-fall-of-fab-com-cautionary-tale-entrepreneur/

- https://medium.com/@schuylerd/launching-sidestage-after-failing-at-my-first-startup-6a1e0dac2c4d

- http://keithbnowak.com/post/55830173333/postmortem-of-my-first-company-a-reposting

- https://medium.com/@nikkidurkin99/my-startup-failed-and-this-is-what-it-feels-like-c5d64b3ae96b

- http://christopherbull.name/2014/06/19/three-years/

- https://www.theguardian.com/technology/2014/may/01/bloom-fm-streaming-music-shuts-down

- http://techcrunch.com/2014/05/09/manilla-shuts-down/

- https://medium.com/@tfridriksson/a-startup-postmortem-with-a-happy-ending-in-thailand-88536216da44

- https://medium.com/@3x14159265/another-catchy-headline-why-you-should-read-this-article-how-my-startup-failed-ef58e3993a1b

- http://telecoms.com/253092/samba-mobile-closes-down/

- http://blog.infotrends.com/?p=14891

- https://medium.com/@jasonhuertas/my-startup-failed-6c54bd68c654

- https://thenextweb.com/apps/2015/03/11/layervault-the-version-control-app-for-designers-is-shutting-down/#.tnw_mDrTqSk4

- https://justinkan.com/exec-cleaning-or-the-challenges-scaling-a-real-world-business-648f3c1898f2

- http://readmill.com/

- http://techcrunch.com/2014/02/16/shutting-down-blurtt/

- http://chrishateswriting.com/post/74083032842/today-my-startup-failed

- http://techcrunch.com/2014/01/21/outbox-shuts-down/

- https://thenextweb.com/insider/2013/12/20/exfm-reveals-shutting-january-15-creates-export-tool-chrome-extension-let-users-keep-data/#.tnw_N0ug3wz9

- https://medium.com/@lazyvalue/bookish-is-a-failing-startup-that-could-fundamentally-change-digital-publishing-d6cbe96c0bd8

- http://www.alleywatch.com/2013/12/tis-the-season-for-a-tigerbow-post-mortem/

- http://www.theverge.com/2013/11/5/5039216/everpix-life-and-death-inside-the-worlds-best-photo-startup

- https://medium.com/@barnettlklane/i-fucked-up-d4b39a515c5b

- http://john.onolan.org/travelllll-post-mortem/

- http://www.shnergle.com/blog/2013/10/23/shnergle-post-mortem/

- https://medium.com/@tomcarra/someone-else-is-building-my-failed-start-up-362826cc23c5

- http://www.recontinued.com/blog/hitmeup-post-mortem

- https://medium.com/@brett1211/postmortem-of-a-venture-backed-startup-72c6f8bec7df

- https://www.linkedin.com/pulse/20130923123247-758147-7-things-i-learned-from-startup-failure

- http://techcrunch.com/2013/09/22/why-startups-fail-a-postmortem-for-social-newsreader-flud-and-what-to-take-from-sonars-demise/

- http://techcrunch.com/2013/08/31/the-decline-and-fall-of-flowtab-a-startup-story/

- https://medium.com/on-startups/5e912a457276

- http://blog.getarkad.com/post/50348770974/lessons-learned-starting-our-first-business

- http://nickfassler.com/2013/05/shutting-down-my-startup/

- http://pando.com/2013/05/22/totsy-burns-through-34-million-lays-off-its-83-employees-selling-assets/

- http://lifescivc.com/2013/04/on-q-ity-a-cancer-diagnostic-company-r-i-p/

- http://insomanic.me.uk/post/48136679276/looking-back-at-7-years-with-my-startup

- http://nemrow.tumblr.com/post/47728450959/my-startup-failed-fuck

- http://blog.capwatkins.com/formspring-a-postmortem

- http://www.abstract-living.com/why-vitoto-failed/

- https://medium.com/work-education/play-by-your-own-rules-6152adc41de9

- http://skillcrush.com/2012/11/14/lessons-from-my-failed-startup-parceld/

- http://www.theverge.com/2014/9/9/6126517/berg-company-behind-little-printer-going-into-hibernation

- http://blog.doddcaldwell.com/post/25472858251/lessons-learned-from-self-funded-startup

- http://techcrunch.com/2012/01/22/post-mortem-for-plancast/

- http://chrishoog.com/the-helloparking-postmortem-a-look-back-and-a-new-perspective/

- http://www.stevepoland.com/the-little-startup-that-couldnt-a-postmortem-of-myfavorites/

- http://www.instigatorblog.com/postmortem-analysis-of-standout-jobs/2010/10/05/

- http://blog.precipice.org/why-wesabe-lost-to-mint/

- http://blog.paulbiggar.com/archive/why-we-shut-newstilt-down/

- https://riotvine.wordpress.com/2010/08/09/post-mortem/

- http://theambitiouslife.com/post/48691070654/youcastr-a-post-mortem

- http://davidcummings.org/2010/06/04/post-mortem-on-a-failed-product/

- http://swapped.cc/certtime

- https://www.crowdfundinsider.com/2016/12/93348-finance-small-companies-still-broken/

- https://www.lily.camera/adventure-comes-end/

- http://tech.economictimes.indiatimes.com/news/startups/home-services-startup-taskbob-shuts-shop/56683800

- https://www.reddit.com/r/changetip/comments/5dn3rc/changetip_shutting_down/

- http://techcircle.vccircle.com/2016/12/19/exclusive-building-materials-marketplace-buildzar-shuts-down/

- http://solidtechnews.com/a-lot-more-wearable-woe-as-vinaya-restructures-and-seeks-pivot-to-b2b/

- http://www.bizjournals.com/boston/news/2017/01/07/after-sinking-on-shark-tank-boston-startup.html

- http://www.mobihealthnews.com/content/open-source-wearable-angel-shuts-down

- https://blog.bitlendingclub.com/2016/12/01/bitlendingclub-closing-soon-due-to-regulatory-pressure/

- https://medium.com/rendeevoo-chronicles/rendeevoo-is-no-more-9425c8cfc64d#.ay50set5b

- http://venturebeat.com/2016/12/29/y-combinator-backed-omniref-is-shutting-down-on-january-31-2017/?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+venturebeat%2FSZYF+%28VentureBeat%29

- https://www.bitphone.net/

- http://the-digital-reader.com/2016/12/28/romance-ebooks-shutting/

- http://opsh.com/2017/01/11/a-final-farewell-from-the-opsh-founders/

- http://icelandreview.com/news/2016/08/31/plain-vanilla-closes-shop-lays-staff?language=en

- http://www.pixelmagegames.com/index.px

- http://www.edmontonsun.com/2016/11/14/alberta-health-services-shuts-down-innovative-meal-sharing-system

- https://medium.com/@jonasboegh/why-were-shutting-down-hivebeat-and-what-we-ve-learned-along-the-way-1b6006101944#.rjxw06plz

- https://medium.com/electroloom-blog/thanks-and-farewell-b0c128c3043f#.q07v6nhu3

- http://www.xconomy.com/wisconsin/2016/07/22/mobileigniter-to-shut-down-after-five-years-and-multiple-pivots/?single_page=true

- http://www.mddionline.com/blog/devicetalk/cms-coverage-decision-killed-my-80m-venture-backed-startup-04-02-15

- https://medium.com/@chloeroose/the-right-words-to-say-goodbye-8a2218b32f92

- https://yourstory.com/2016/04/peppertap-journey-navneet-singh/

- http://www.forbes.com/sites/forbestreptalks/2016/05/24/how-dinner-lab-blew-through-10-million-on-a-failed-restaurant-startup/2/#10a04f486a5a

- https://www.edsurge.com/news/2016-06-12-we-shut-down-our-edtech-startup-here-s-what-we-learned

- https://techcrunch.com/2016/03/21/identity-verification-startup-jumio-files-for-bankruptcy-will-sell-assets-to-early-backer-eduardo-saverin/

- http://www.betaboston.com/news/2015/10/06/after-laying-off-most-of-its-staff-clothing-resale-startup-fashion-project-regroups/

- http://postghost.com/Home/Shutdown/

- https://medium.com/@tmzier/why-zen99-shut-down-a368371eb9dd

- http://www.greentechmedia.com/articles/read/QBotix-Robotic-Solar-Tracking-Fails-to-Reach-the-Market

- https://medium.com/startup-study-group/inside-story-of-vatler-s-shut-down-8c42bad83f09

- http://www.forbes.com/sites/davechase/2015/10/05/lessons-from-mayo-backed-better-shutting-down/

- http://venturebeat.com/2015/07/13/chat-app-kato-will-shut-down-on-aug-31-because-slack/

- http://patterbuzz.com/2015/03/down-but-not-out/

- http://techcircle.vccircle.com/2015/01/06/private-label-fashion-e-tailer-donebynone-goes-down-investor-says-relaunching-with-new-team/

- http://blog.brawker.com/post/116408675050/brawker-shuts-down

- https://www.balancedpayments.com/stripe

- http://www.bizjournals.com/boston/blog/startups/2015/03/funding-woes-cause-subscription-based-fashion.html

- http://whyownit.com/blog/we-failed-warum-die-verleih-app-why-own-it-nicht-funktioniert-hat

- http://cointelegraph.com/news/114148/melotic-exchange-shuts-down-cnet-founder-wants-to-bring-bitcoin-to-india

- http://www.theverge.com/2015/4/30/8526105/grooveshark-shuts-down-settles-with-labels

- http://om.co/2015/03/09/a-statement-about-gigaom/

- http://digitalroyalty.com/digital-royalty-news-hanging-up-the-crown/

- http://www.bizjournals.com/newyork/news/2015/08/10/david-bloom-ordrx-google-ventures-patent-troll.html

- http://www.nextbigwhat.com/talentpad-shutdown-297/

- http://thisismyjam.tumblr.com/post/126260430022/jam-preserves

- http://www.finextra.com/news/announcement.aspx?pressreleaseid=60844

- http://gamasutra.com/blogs/IvanMir/20150217/236560/Postmortem_Traps_for_Friends__our_attempt_at_fair_IAP_multiplayer.php

- http://www.quora.com/Why-do-customization-startups-fail

- http://blog.getbackchat.com/post/88313702290/the-end-of-a-great-experience

- https://www.side.cr/why-we-sold-to-gm/

- http://blog.bergcloud.com/2014/09/09/week-483/

- http://blog.wishberg.com/post/92014031388/the-final-note-thanks-from-team-wishberg

- http://medcitynews.com/2016/01/healthspot-fail-telemedicine/

- http://blog.flytenow.com/the-beginning-of-the-end

- http://www.businessinsider.com/london-hotel-ranking-startup-top10-raised-12-million-in-funding-but-now-its-shutting-down-2015-12

- http://venturebeat.com/2015/12/11/prismatic-is-shutting-down-its-news-app-for-ios-android-and-web-on-december-20/

- http://techcrunch.com/2015/12/30/att-snaps-up-assets-talent-from-carrier-iq-as-phone-monitoring-startup-goes-offline/

- http://www.coindesk.com/bitcoin-startup-bonafide-shuts-down/

- http://techcrunch.com/2015/11/25/dineins-last-supper/

- http://nymag.com/daily/intelligencer/2015/09/they-were-quirky.html

- http://novobrief.com/selltag-shuts-down/

- https://www.techinasia.com/millions-bank-saif-partnersbacked-gozoomo-shuts-shop-heres-happened

- http://venturebeat.com/2016/10/13/game-engine-startup-maxplay-confirms-near-total-layoffs-and-switch-to-licensing/

- http://blog.vrideo.com/taking-our-goggles-off/